IRS Back Taxes Guide

The Ultimate Guide to

Resolving IRS Back Taxes

It starts with a single, unopened letter. Then another. Soon, there’s a small, daunting pile of mail from the IRS that you’ve strategically placed in a drawer, hoping it might somehow magically vanish. The feeling is a familiar one for millions of Americans. A quiet, persistent dread that hums in the background of daily life. You wonder what the IRS might do next, and the thought of figuring it all out feels so overwhelming that it’s easier to just … not.

That weight you’re feeling? You can lift it. Facing the IRS is never as scary as the uncertainty of ignoring the problem. There is a clear, well-trodden path to resolving back taxes, and you have more control over the situation than you might think.

This guide is your roadmap. We’re going to walk you through why people fall behind on their taxes (you’re in good company, believe us), what happens when you don’t file, and the step-by-step solutions available to put you back in control and on the path to becoming debt-free.

Why People Fall Behind on Taxes: You’re Not Alone

If you’ve fallen behind on your taxes, you are not a bad person. You’re just a person who has had… well, life happen. It turns out that life is often messy and rarely consults the tax code before throwing a curveball. Here are some of the most common reasons good people get on the wrong side of the IRS.

- Life Throws a Wrench in the Works

A sudden job loss, a divorce, an unexpected medical emergency, or the death of a loved one can turn your financial world upside down. When you’re focused on navigating a crisis, filing taxes is often the last thing on your mind.

- The Surprises of Self-Employment

If you’ve recently ventured into the world of freelancing or started your own business, you’ve probably discovered the less-than-joyful reality of self-employment taxes and the quarterly estimated payments that go with them. It’s a classic case of “you don’t know what you don’t know,” and it can lead to a shocking tax bill you’re simply not prepared for.

- Fear of a Small Bill Becoming a Big One

Sometimes, it starts with a single tax bill you can’t afford to pay. So you put it off. Then, penalties and interest begin to pile up, and the number grows larger and more daunting. It’s a classic case of procrastination fueled by anxiety, and it can make you feel like you’re trapped in a financial snowball fight where you’re the only target.

- Missing Pieces of the Puzzle

You can’t file what you can’t find. Whether it’s a lost W-2 from a job you had for three months or a 1099 that never showed up in the mail, missing documents can bring your tax preparation to a screeching halt.

The Consequences of Ignoring the IRS

Here’s the thing about tax problems: they don’t get better with age. Ignoring the IRS is akin to ignoring a leaky faucet. It starts as a small drip, but eventually, it can cause significant damage. The key is to understand the consequences without letting them paralyze you with fear.

The Snowball Effect

The IRS has two main penalties that can make your tax debt grow surprisingly fast: the failure-to-file penalty and the failure-to-pay penalty.

- The failure-to-file penalty is the big one. It can be up to 5% of your unpaid taxes for each month your return is late.

- The failure-to-pay penalty is smaller, at 0.5% per month.

The lesson here? Even if you can’t pay a dime, you should always, always file your tax return on time. Additionally, the IRS charges interest, which compounds daily on your tax, penalties, and the interest that has already been added. It’s how a manageable tax debt can become a monster over time.

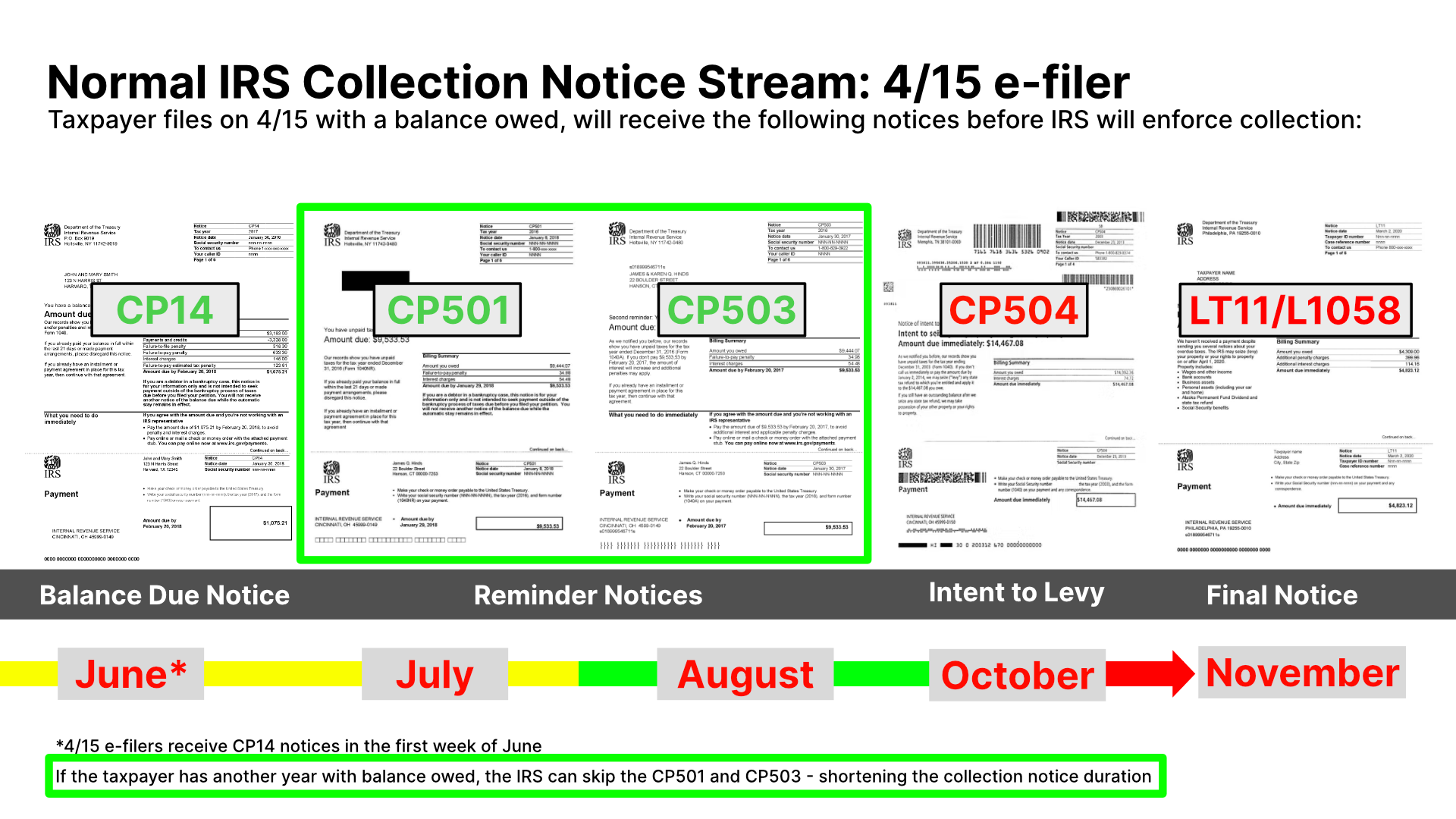

The IRS Collection Process

If you don’t file a return, the IRS won’t just forget about you. Eventually, they may file a Substitute for Return (SFR) on your behalf. This sounds helpful, but it’s really not. The IRS will typically only give you the most basic deductions, which usually results in a much higher tax bill than if you had filed yourself.

If you continue to ignore the problem, the IRS can move on to more serious collection actions, such as:

- A Federal Tax Lien: This is a legal claim against all your current and future property, like your house or your car. It’s a public record, so it can make it incredibly difficult to get credit.

- A Tax Levy: This is when the IRS actually seizes your property to pay your tax debt. They can take money directly from your bank account, garnish your wages, or even seize and sell your assets.

The first step toward resolving your tax debt is filing all past-due returns to become compliant.

This can be a complex process, especially if you're missing records. Our team can retrieve your IRS transcripts and prepare your back taxes accurately to stop escalating penalties and open the door to a resolution.

Your First Step to Freedom: Becoming Compliant

So, how do you stop the snowball and start moving toward a solution? The very first step, before you do anything else, is to get back into good standing with the IRS. This is what’s known as “becoming compliant.”

How Many Years Do I Need to File?

Generally, the IRS requires you to file the last six years of delinquent tax returns to be considered compliant. Once you've done that, you open the door to all the available resolution options.

But I Don’t Have My Old Tax Documents!

This is a common and very solvable problem. The IRS keeps records of all the income reported under your Social Security number. You can request a Wage and Income Transcript from the IRS for free, which will show you all the information from your old W-2s, 1099s, and other tax forms.

Prepare and File the Returns

The most important thing is to file accurately. This is your chance to claim all the deductions and credits you’re entitled to, which can significantly lower your tax bill. And remember, filing your return stops the costly failure-to-file penalty and starts the 10-year clock on the statute of limitations for the IRS to collect the tax from you.

The Solutions

How to Resolve Your Back Tax Debt

Once you’re compliant, you can start working on a solution to pay off your debt. The good news is that the IRS offers several programs specifically designed to assist individuals in your exact situation.

- Option 1: IRS Installment Agreement (IA)This is for people who can afford to pay their full tax debt, just not all at once.

An Installment Agreement is a monthly payment plan that you set up with the IRS. If you owe less than $50,000 in combined tax, penalties, and interest, you can set up a streamlined agreement and take up to 72 months to pay it off.

- Option 2: Offer in Compromise (OIC)This is for individuals who genuinely cannot afford to pay their full tax debt due to their financial circumstances.

An OIC is an agreement with the IRS to settle your tax debt for less than the full amount you owe. The IRS will look at your ability to pay, your income, your expenses, and the equity in your assets to determine if you’re a good candidate. This is a powerful solution, but the qualification process is rigorous.

- Option 3: Currently Not Collectible (CNC) StatusThis is for individuals experiencing severe financial hardship who are currently unable to make any monthly payments.

If you’re approved for CNC status, the IRS will temporarily pause all collection efforts, like levies and wage garnishments. Your debt doesn’t go away, and interest will continue to accrue, but it gives you breathing room until your financial situation improves.

- Option 4: Penalty AbatementThis is for individuals who have a legitimate reason for their tax issues or a history of timely filing and payment.

The IRS may agree to remove penalties if you can show you had a “reasonable cause” for not filing or paying on time (like a serious illness or a natural disaster). You might also qualify for the First-Time Abatement program if you have a clean three-year compliance history.

- Option 5: BankruptcyThis is an option for people with overwhelming debt that goes beyond just taxes.

In some cases, older income tax debts can be discharged through Chapter 7 bankruptcy, but there are stringent rules you have to meet. The moment you file for bankruptcy, an “automatic stay” goes into effect, which immediately stops all IRS collection actions.

Choosing between an Installment Agreement, an Offer in Compromise, and other programs is a critical decision.

Each solution has strict and complex eligibility rules. Let our experts analyze your specific financial situation to determine the most effective resolution strategy available to you.

Take the First Step Today

The journey from tax debt to financial freedom can seem daunting, but it all begins with a single, straightforward step: filing your past-due tax returns. No matter how big the number on those IRS letters seems, and no matter how long you’ve been avoiding it, there is always a solution available. The key is to stop worrying and start doing.

Feeling overwhelmed? You don’t have to figure this out alone. Schedule a free, confidential consultation with TaxSolve today to understand your options and create a plan to put your tax problems behind you for good.